KYC & Compliance: Using AI to Verify Customer Documents

In an age of deepfakes and digital fraud, compliance teams are under pressure to verify customer documents more effectively than ever. KYC regulations and requirements apply to almost all institutions that deal with money, including banks, financial services providers, and non-financial sectors. Manual checks and static rules struggle to keep up with increasingly sophisticated forgeries. KYC standards are designed to protect financial institutions against fraud, corruption, money laundering, and terrorist financing, and KYC processes are employed by companies of all sizes and in all industries to ensure their customers are who they claim to be and to assess risks. The KYC process involves the verification process for account owners, generally requiring KYC documents such as government-issued IDs and proof of address to confirm identity and address. The Customer Identification Program (CIP) requires financial institutions to verify the identity of anyone looking to open an account, further strengthening compliance requirements. KYC checks aim to prevent business relationships from being established with persons associated with terrorism, corruption, or other illicit activities, and effective KYC protects organizations from reputational damage associated with criminal activities. Non-compliance with KYC regulations resulted in over $4.3 billion in penalties for U.S. financial institutions in 2024. KYC regulations have evolved from simple identity verification into comprehensive risk management frameworks designed to prevent illicit financial activity. AML regulations are integrated within the broader framework of KYC procedures, ensuring compliance with anti-money laundering standards and helping organizations meet regulatory compliance requirements. This post explores how artificial intelligence is transforming Know Your Customer (KYC) document verification – improving accuracy, speed, and consistency for compliance officers, risk teams, fintechs, and any business that relies on customer-submitted documents.

Why Document and Identity Verification Is Central to KYC Compliance

Customer-submitted documents – from passports and ID cards to utility bills, bank statements, and accompanying documents – form the backbone of KYC compliance. Common KYC documents required by law include government-issued IDs such as a driver's license, as well as proof of address and financial records. Verifying these documents is how businesses know their customer and ensure a person or business is legitimate. The verification process is essential for identity validation, compliance, and fraud prevention. Regulators worldwide require that institutions collect and accurately verify identity documents, proof of address, financial records, and more. Confirming identity typically involves government-issued IDs and additional documents to ensure accuracy. Manual verification is often used to cross-check documents and data sources, especially in later stages of onboarding, to prevent fraud and ensure regulatory compliance. Reasonable diligence is necessary for brokers and financial institutions to verify customer identities and adhere to regulations. KYC processes typically include document verification, face verification, and address verification as part of the identity verification process. Reported fraud losses increased by 25% to $12.7 billion in 2024, highlighting the need for robust verification through KYC. Failure to do so can lead to dire consequences. If a fake or altered document slips through, it opens the door to fraud, money laundering, and compliance violations. The fallout from weak document verification can include multi-million dollar fines, criminal liability for negligence, and severe reputational damage. In other words, robust document checks aren’t just bureaucracy – they are a frontline defense against financial crime and a means to avoid regulatory penalties.

Consistent and thorough document verification also builds trust. When customers know their identities and documents are being handled with care, they feel safer. And when regulators audit a company’s KYC program, they expect to see that documents (like IDs and certificates) were verified accurately and consistently. In short, document verification is central to both regulatory compliance and risk management – it’s where you prove that “John Doe” is who he claims, that a business exists legally, and that nothing fraudulent is being used to open accounts or access services.

How AI Improves Customer Document Verification

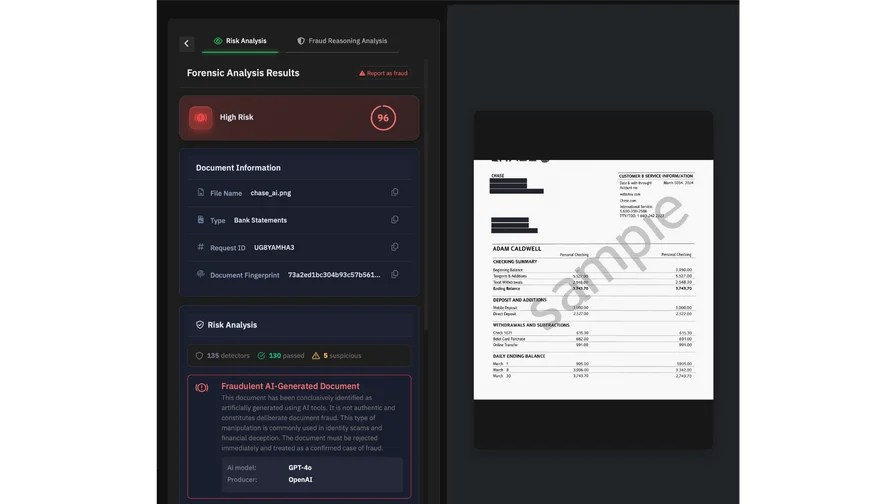

AI-powered document verification tools analyze digital documents and flag even subtle signs of tampering. The example above (from an AI document checker) shows how the system can distinguish a trusted document versus one with a high risk of fraud by examining everything from font consistency to editing metadata. These models inspect elements like text fonts, timestamps, and software signatures that would be invisible to manual reviewers. This process, known as automated verification, streamlines document processing by enabling real-time decision-making and improving both efficiency and compliance.

AI changes the game by bringing speed, consistency, and depth to document analysis. Instead of relying on a human’s eyes, AI algorithms examine documents pixel by pixel and byte by byte. They don’t get tired or rushed. An AI can parse the structure, layout, fonts, and metadata of a document far more thoroughly than a person can. For example, AI will analyze if the font used in a bank statement’s text is perfectly uniform, or if one line of text was copy-pasted in a slightly different font – a subtle sign of tampering that a human might miss. It will check metadata like creation timestamps and software tags to see if, say, an “official PDF” was oddly edited with an image editing program (a red flag). By inspecting details such as document format consistency, image artifacts, digital signatures, and hidden fields, AI can detect alterations invisible to the human eye. In contrast, manual verification relies on labor-intensive cross-checking of documents and data sources, which can be inconsistent and slower, making it harder to keep up with high volumes and sophisticated fraud attempts.

Another huge advantage is that AI-driven verification is consistent and repeatable. The same document will get the same treatment every time, without the variability of different reviewers. This removes subjectivity – decisions are based on data and learned patterns. If a document is suspicious, the AI will flag it no matter who submits it or when. Conversely, if it’s truly authentic, AI is less likely to raise a false alarm due to fatigue or bias. AI systems are trained on vast datasets of both genuine and fake documents, which means they learn to recognize patterns of forgery. Over time, as they process more data, they actually improve (machine learning models get “smarter” with experience). They can spot anomalies like a mismatched font, an incorrect layout, or a missing security feature across millions of documents with unwavering attention. In the context of KYC verification, AI enhances the accuracy and consistency of the verification process, reducing errors and improving customer experience. Automation in KYC processes allows for the evaluation of significantly more applicants without sacrificing compliance standards. The shift towards eKYC and automated AI-driven solutions is transforming onboarding by streamlining procedures and ensuring compliance with global regulatory standards.

Scalability is another benefit. AI verification operates in seconds, not hours. A machine can process thousands of documents in the time it takes a human to manually inspect one. This means compliance teams can handle volume spikes (like a surge of new account openings) without compromising on thoroughness. And they can do so 24/7 – AI doesn’t need sleep. When it comes to evolving fraud patterns, AI can adapt faster too. Models can be updated or retrained to recognize new types of fakes, whereas updating a rules-based system or retraining dozens of human staff is much slower. In sum, AI brings a superhuman ability to analyze documents deeply and consistently at scale. It catches the doctored details and synthetic forgeries that humans miss, and it delivers decisions in real time, enabling compliant but frictionless onboarding. By using AI, compliance teams get accurate, repeatable verification decisions at scale, transforming document checks from a bottleneck into a strength.

AI in Practice: What It Verifies in Customer Documents

AI doesn’t just work in theory – in practice it’s verifying all the same documents that compliance teams deal with daily, but with far greater scrutiny. Here are some key document types and how AI tackles them:

- Identity Documents (Passports, IDs, Driver’s Licenses): AI-powered verification can authenticate government-issued IDs by analyzing security features and layout. It can verify the text on an ID (names, dates, ID numbers) via OCR and confirm it matches the expected format. It examines visual features like holograms, watermarks, and microprint patterns if available, and flags if something is off. For example, AI can detect if a passport photo was digitally altered or if an ID’s machine-readable zone (MRZ) code doesn’t match the printed info. It cross-checks the document against known templates for that country/issuer, so a fake that deviates in design will be caught. Essentially, AI looks for any sign that an identity document isn’t genuine – from altered headshots to fonts that aren’t consistent with the real thing. This verification process is required for account owners and must include key information such as date of birth to comply with regulatory standards.

- Proof of Address Documents (Utility Bills, Bank Statements, Rental Agreements): These are commonly forged with simple edits (changing a name or address on a legitimate bill) or using templates. AI shines here by detecting altered data and reused templates. It will notice if the text alignment or font on one line (say, the address line) is slightly different – a clue that someone swapped in new text. It checks if logos, formatting, and barcodes match what a real utility bill from that provider should look like. Some AI systems even compare the content against databases (for instance, does the postal code exist in the city stated?). By analyzing formatting consistency and metadata, AI can tell if a PDF bill was generated by an official utility company or edited manually afterwards. Any little inconsistency – an odd shadow behind text, mismatched spacing – can reveal a fake, and AI will catch it.

- Financial and Business Documents (Bank Statements, Pay Slips, Tax Records, Business Licenses): Fraudsters often doctor financial documents to inflate income or create companies on paper. AI verification validates these documents by ensuring all pieces line up logically. It can recalc totals on a payslip or invoice to see if someone altered an amount without updating the sum. It checks if account numbers or tax identifiers follow the correct format. AI also spots template forgeries – for instance, if multiple applicants submit bank statements that look identical aside from the names and numbers, that’s a red flag (it suggests a common template was used). AI can maintain a database of known genuine document layouts and compare incoming documents to them. If a submitted document deviates from the known authentic pattern in ways it shouldn’t, or conversely if it matches too perfectly a known fake template, the system will flag it. In short, AI digs into the content and context: verifying that figures make sense, that dates haven’t been tampered with, and that each document makes sense for what it claims to be.

Financial services providers, including banks and other financial institutions, are required to perform these checks as part of regulatory compliance. The Customer Identification Program (CIP) requires financial institutions to verify the identity of anyone looking to open an account.

Across all these document types, AI is looking for signs of alteration, fabrication, or inconsistency. That could be as blatant as data that doesn’t match (e.g. an ID number that isn’t valid), or as subtle as a slight blurring around text (indicating it was Photoshopped). The power of AI is that it applies dozens of forensic checks in parallel – far beyond the handful of things a human might remember to look for. Did someone use an editing tool on this PDF? AI will detect software edit signatures embedded in the file. Is the font in this scanned paystub exactly the same as genuine ones? AI will compare it to known samples. By verifying IDs, addresses, and financials with such granularity, AI helps ensure that every document is authentic and unaltered. Altered data, reused templates, fabricated records – all are uncovered by AI’s pattern recognition and cross-checks, whereas they might easily slip past a cursory manual review.

eKYC systems often combine ID document verification, biometric authentication, and real-time risk monitoring to authenticate users. Entrust offers a comprehensive identity verification solution to simplify the verification process for customers.

Anti-Money Laundering: AI’s Role in Preventing Financial Crime

Artificial intelligence is rapidly transforming the fight against financial crime, especially in the realm of anti-money laundering (AML). For financial institutions, the stakes are high: failing to detect and prevent money laundering or terrorism financing can result in severe regulatory penalties and reputational harm. AI-driven analysis empowers compliance teams to identify suspicious transactions and patterns that might otherwise go unnoticed, significantly enhancing the effectiveness of the AML process.

By leveraging machine learning algorithms and natural language processing, AI systems can sift through vast amounts of transaction data, customer profiles, and external intelligence to flag anomalies in real time. This not only improves the accuracy of customer due diligence but also streamlines the overall KYC process, allowing financial institutions to focus their resources on the highest-risk cases. AI-powered AML solutions can help organizations meet the stringent requirements set by regulatory bodies such as the Financial Industry Regulatory Authority (FINRA), ensuring that every step of the KYC process is both thorough and compliant.

Moreover, AI’s ability to adapt and learn from new data means that financial institutions can stay ahead of evolving money laundering tactics. By integrating AI into their AML and KYC workflows, organizations can reduce fraud risks, enhance due diligence, and protect both themselves and their customers from financial crime.

Enhanced Due Diligence: Addressing High-Risk Customers with AI

Enhanced due diligence (EDD) is a vital part of the KYC process, especially when financial institutions are dealing with high-risk customers or complex ownership structures. Traditional EDD can be resource-intensive, requiring deep investigation into beneficial owners, source of funds, and potential links to financial crime. AI technology is revolutionizing this process by enabling compliance teams to analyze large volumes of identity data, transaction histories, and external databases with unprecedented speed and accuracy.

AI-powered EDD solutions can automatically verify the identities of beneficial owners, conduct comprehensive sanctions and watchlist screening, and monitor customer activity for signs of suspicious behavior. This not only helps financial institutions meet their due diligence obligations but also ensures that high-risk customers are identified and managed appropriately. By automating much of the data gathering and analysis, AI allows compliance teams to focus on the most complex cases, improving both efficiency and effectiveness.

Importantly, AI-driven EDD helps financial institutions strike the right balance between robust risk management and a seamless customer experience. Customers benefit from faster onboarding and fewer manual checks, while institutions gain deeper insights into potential risks—ensuring that their KYC process is both thorough and customer-friendly.

Challenges of Implementing KYC with AI

While the benefits of AI in the KYC process are clear, implementing these technologies comes with its own set of challenges. One of the primary concerns is ensuring that AI systems are trained on high-quality, representative data to avoid bias and minimize errors in customer verification. Financial institutions must also ensure that their AI-powered KYC solutions comply with all relevant regulatory requirements, particularly those related to data protection and customer privacy.

Integrating AI technology with existing workflows and legacy systems can be complex and resource-intensive. It often requires significant investment in both technology and staff training to ensure a smooth transition. Additionally, the explainability and transparency of AI-driven decisions are critical—compliance teams need to understand and justify why a particular customer or document was flagged, both for internal governance and regulatory scrutiny.

To address these challenges, financial institutions should adopt a thoughtful approach to AI implementation, prioritizing transparency, regulatory compliance, and seamless integration with existing workflows. By doing so, they can harness the power of AI while maintaining the trust of customers and regulators alike.

What to Look for in an AI Document Verification Solution

Not all AI solutions are created equal. Compliance teams shopping for an AI-driven document verification tool should keep several key criteria in mind to ensure the technology truly meets their needs. The verification process is a critical component of customer onboarding, as it validates identities, ensures compliance, and helps prevent fraud—making it essential to select an AI solution that excels in this area. KYC processes are employed by companies of all sizes to ensure their customers are who they claim to be and to assess risks:

- Accuracy and Coverage Across Document Types: Look for a solution proven to accurately handle the range of documents you encounter – from various national ID formats and passports to different kinds of financial statements and letters. The AI should have been trained on diverse document types and formats (PDFs, images, scans, etc.) so that it can identify and verify documents from different countries and sources with high precision. In short, it needs a broad knowledge base. A good sign is if the provider can cite accuracy rates (e.g. 98-99% accuracy) on test sets and support multiple document classes. The system should also support high-resolution image input and detect forgeries in both color scans and black-and-white photocopies. Accuracy isn’t just about catching fakes – it’s also about correctly recognizing genuine documents to minimize false rejects. So seek out solutions with a strong track record across the board.

- Detection of Both Simple and Advanced Fraud: Your AI tool must be adept at catching the full spectrum of fraud, from the obvious to the very subtle. Basic tampering (like edited text or a replaced photo) should be table stakes – the AI should flag any signs of image manipulation, text overlays, mismatched fonts, or erased/retyped areas. But beyond that, ensure the system can detect advanced forgeries: things like AI-generated documents, synthetic identities, or “too-perfect” template copies. Ask if it uses techniques to identify deepfake images on IDs or if it can spot when multiple different documents use the same template (indicating a common source of fraud). The solution should have layers of analysis – checking document layout integrity, verifying security features, analyzing metadata, and using anomaly detection to catch things that “just don’t add up.” Fraud tactics will continue to evolve, so the AI needs to be one step ahead. Ideally, the provider updates the models regularly as new fraud patterns emerge. Future-proofing against novel attack techniques is critical; you want an AI that’s as agile and adaptive as the fraudsters.

- Integration with Existing Workflows: In a compliance environment, new tech has to play nicely with your current systems. Look for AI verification solutions that offer easy integration – whether via APIs, SDKs, or built-in workflow tools. The solution should be able to plug into your onboarding or compliance software so that when a customer uploads a document, it automatically gets analyzed by the AI and returns a result in real-time. Nobody wants a stand-alone system that doesn’t talk to your customer management platform or case management system. Check if it supports outputting structured results (like JSON or PDF reports of the analysis) that can feed into your case workflow. Also consider whether the AI can be customized or tuned to your policies – for example, adjusting confidence score thresholds for flags, or integrating with your internal databases for cross-referencing. A good AI document verification tool will advertise quick deployment and compatibility with common platforms. In essence, it should enhance your existing KYC/AML workflow, not disrupt it. Seamless integration ensures you get the efficiency gains without needing to overhaul your entire tech stack.

- Data Security and Privacy Compliance: Since customer documents contain sensitive personal information, any AI verification solution must handle data with the highest security standards. Prioritize vendors that are ISO 27001 certified, SOC 2 compliant, or have similar security attestations. This indicates they follow strict information security practices. The solution should use encryption for data in transit and at rest. It’s also important to know whether the tool stores any documents or data – many compliance teams prefer solutions that do not retain documents longer than necessary, to reduce risk. Some AI document checkers will process documents in memory and return a result without saving the file. Ensure the solution allows you to comply with privacy laws like GDPR; for example, if you operate in the EU, you might need EU data residency or specific contractual clauses in place. If using a cloud-based AI service, consider where the servers are located. Regional compliance considerations are key – the provider should be able to accommodate data handling requirements in different jurisdictions (or offer on-premise deployments if needed for privacy). In short, verify that the AI not only catches fraud but also protects your customers’ data and meets any regulatory privacy obligations you have.

- Transparency and Explainability: It might not be explicitly listed on every brochure, but it’s wise to choose an AI solution that offers clear explanations for its decisions. In practice, this means the tool should be able to show or tell you why it flagged a document as fraudulent (e.g. highlighting the area that was altered or noting “font mismatch in date field”). This feature is invaluable for your compliance team to understand and trust the AI’s output, and it’s a huge plus if you need to present findings to regulators or auditors. An AI that’s a complete black box can be problematic in compliance. Many top solutions provide a detailed report or interface indicating the checks performed and results (for example, “Document modified after creation – metadata timestamp mismatch” or “Suspicious software used to edit PDF” with high certainty). These breadcrumbs help your human analysts quickly validate the AI’s conclusions and take action. So, prioritize a solution that offers explainable results and user-friendly reports, rather than one that just spits out a cryptic score.

By evaluating solutions against these criteria – accuracy, fraud detection depth, integration, security, and transparency – you’ll be better positioned to choose an AI document verification platform that truly strengthens your KYC and compliance program. Remember, the goal is to find a tool that boosts your confidence in the documents you’re processing while fitting neatly into your operational puzzle. Don’t hesitate to ask vendors for proof of their accuracy (benchmark results), details on how they detect advanced fraud, client references, and documentation on their security measures. The right solution will make document verification faster and more reliable, all while keeping regulators happy and fraudsters at bay. As financial services become increasingly digital, the adoption of eKYC procedures has accelerated globally, making robust and automated verification processes more important than ever.

Best Practices for KYC in the Age of AI

To achieve successful KYC compliance in today’s AI-driven landscape, financial institutions should adopt a set of best practices that ensure both regulatory compliance and a positive customer experience. First, implementing a risk-based approach to the KYC process is essential—this means applying enhanced due diligence to high-risk customers while streamlining verification for lower-risk profiles. AI technology can be leveraged to automate and optimize these processes, but it’s crucial that AI systems are regularly validated, monitored, and updated to maintain accuracy and fairness.

Seamless integration with existing workflows is another key best practice. AI-powered KYC solutions should work in harmony with current systems, enabling real-time document verification and customer identification without disrupting operations. Transparency is equally important: financial institutions should provide clear explanations for AI-driven decisions, ensuring that both customers and regulators understand the rationale behind each outcome.

Ongoing monitoring and continuous training of AI systems are vital to keep pace with evolving fraud risks and regulatory requirements. By prioritizing these best practices—risk-based due diligence, automation, integration, transparency, and ongoing monitoring—financial institutions can build KYC processes that are not only compliant and secure but also efficient and customer-centric. This approach positions organizations to meet their KYC obligations confidently, even as the regulatory and technological landscape continues to evolve.

Conclusion

It’s clear that AI has moved from a “nice-to-have” to a core layer of any modern, document-heavy KYC process. AI significantly enhances the verification process, making it faster, more accurate, and more reliable for companies of all sizes. Given the scale and sophistication of today’s document fraud, relying solely on manual checks or outdated systems is simply no longer viable. AI-driven document verification has proven it can handle the heavy workload – parsing countless IDs and records in seconds – and do so with a level of accuracy and consistency humans can’t match. This isn’t about replacing compliance teams, but empowering them. With AI, compliance officers can trust that every uploaded document is vetted against dozens of criteria instantly, allowing them to focus their expertise where it’s truly needed (like investigating complex cases and making judgment calls). The end result is a compliance workflow that is both scalable and robust – ready for the future.

Document verification sits right at the frontline of defense against fraud. It’s during onboarding or account opening that you have the best chance to catch a fake ID or a forged bank statement before it causes downstream damage. AI fortifies this frontline. It ensures that fraudulent documents are caught at the gate, protecting the institution from bad actors sneaking in with forged credentials. At the same time, it lets honest customers through more quickly, improving their experience. Businesses that embrace AI for KYC find they can onboard customers faster and more accurately – turning compliance into a competitive advantage rather than a bottleneck. They win customer trust by providing a smoother process and win regulator trust by demonstrably tightening controls.

Importantly, AI makes your compliance program future-proof. Fraud techniques will keep evolving (who knows what fake document scheme will surface next year), but an AI system can learn and adapt to new patterns far more rapidly than manual processes can. It provides a kind of “continuous intelligence” layer to KYC. Rather than static one-time checks, you have an ever-watchful system that improves with each document it sees. This kind of resilience is exactly what regulators are starting to expect – proactive, technology-enhanced compliance that can adjust in real time to new risks.

In conclusion, leveraging AI for document verification isn’t about abandoning the human element or cutting corners – it’s about augmenting the KYC process to meet the realities of the digital age. By making AI a core layer in their compliance stack, organizations can fight fraud more effectively, streamline their operations, and maintain the trust of customers and regulators alike. In a world where a fake document can be a few clicks away for criminals, AI is rapidly becoming an indispensable ally in keeping our financial systems secure and compliant. The message is clear: for document-heavy workflows, AI isn’t optional anymore – it’s the key to scalable, reliable, and future-ready KYC compliance.